By Michael Irgang, Global Risk Management Inc.

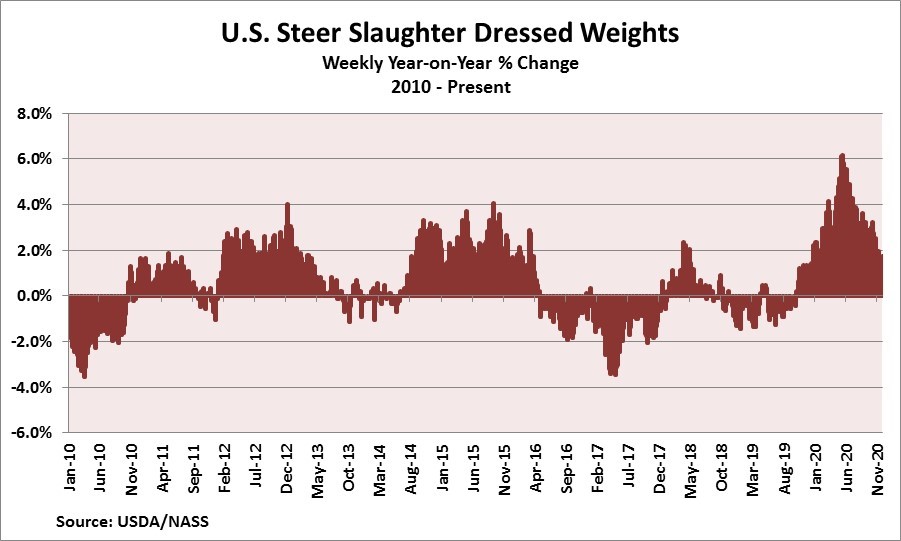

The U.S. beef industry faced widely publicized production challenges in 2020, largely due to COVID-19-related issues at the packing plants. One positive for U.S. beef production was elevated dressed weights for fed cattle coming off of feedlots to be marketed to packing plants. While total cattle slaughter for 2020 was down 3.5% at 31.7 million head, total beef production was down only 1.0% at 26.4 billion lbs. largely due to higher cattle weights. The average dressed weights for steers reached 931 lbs./head for the week ended October 24th, 2020, the highest weekly average weight on record in the USDA’s data series. Interestingly, the increase in cattle weights in 2020 enabled the production of over 630 million additional pounds of meat above and beyond what would have been produced had 2020 dressed weights been unchanged for 2019. Arguably the most impressive statistic is that weekly cattle weights have been higher year-on-year since the week of October 14th, 2019. The question on the minds of people in Foodservice, Retail, Packing Plants and Further Processing Facilities is how long will this trend continue?

To answer this question, the following factors will be closely watched to determine the direction of fed cattle weights and ultimately U.S. beef production in 2021:

1.) Feedlots Have Become More Current: The temporary shutdowns of U.S. packing plants last Spring led to an increase in cattle being significantly backed up on feedlots, leading producers to feed cattle to higher weights until slaughter capacity returned. According to USDA data, the number of cattle on feed in the ‘150+ day’ category as of June 1st, 2020 was 3.3 million head, or 41% of the total on feed number for the month and a record for the month. By November 1st, 2020, the number of cattle in the ‘150+ day’ category had fallen to 2.1 million head, which is a more normal level of 18% of the total ‘on-feed’ number.

2.) Cost of Gain: Feedlot operators look closely at the cost of adding incremental pounds to fed cattle when making their feeding decisions, which is known as the Cost of Gain (COG.) With grains prices surging in recent weeks, we are estimating that feed costs for fed cattle will increase 18%+ during 2021, which will lead producers to market their livestock at lower weights, absent a meaningful rally in live cattle prices. Another potential drag on live weights is the reduced use of beta agonists by feedlot operators in their feed rations. Beta agonists (i.e. Optaflexx) are feed additives that allow for the efficient addition of weight during the final 30 days cattle are on feed, but their use is banned in several exports markets. With U.S. beef exporters eyeing some of the markets that ban beta agonists, their usage will likely decrease and put downward pressure on fed cattle weights.

3.) Slaughter Mix: The slaughter mix between heifers and steers impacts dressed weights for fed cattle because heifers in U.S. feedlots weigh, on average, 69 pounds/head less than steer. During the plant shutdowns last Spring, many feedlots increased the percentage of steer in their slaughter mix, thus raising total dressed weights. In 2021, a normalization of the slaughter mix to increase the percentage of heifers will bring weights down.

4.) Weather: Weather is a major wildcard that can greatly influence dressed weights and ultimately beef production. During winter months when the Plains states experience abnormally cold weather and/or elevated precipitation, feedlot productivity will be negatively impacted. The winter of 2018 was a textbook example in which heavy precipitation in part of the Plains led to dressed weights 10 – 15 lbs./head lower than the prior year for several weeks. Looking into early 2021, we currently see no weather patterns developing which would hamper feedlot productivity, but of course this outlook could change quickly.

On balance, we believe that the factors above individually and collectively will lead dressed weights for fed cattle lower in the months to come. The question is one of degree, so the above points will be closely monitored. We are aware of feedlots that have residual stocks of fed cattle at higher weights yet to be marketed, which will keep dressed weights buoyed in the very near term. Going into mid-February, weights are likely fall due to any one or more of the factors mentioned above. The USDA’s Supply & Demand Estimate Report released earlier this week pegged 2021 U.S. beef production at 27.259 billion lbs., a decrease of 70 million pounds from the November estimate and 297 million pounds below the original estimate released in May 2020. GRM’s firm view is that U.S. beef production will continue to be revised downward over the next several months, and lead to tighter overall supplies of beef in 2021.

Commodity trading is not suitable for all investors. There is an inherent risk of loss associated with trading commodity futures and options on futures contracts, even when used for hedging purposes. Only risk capital should be used when investing in the markets. Past performance is not indicative of future results.